All Topics / General Property / The History of Australian property values

- alfrescodining wrote:Look from 1990 onwards.

Interest rates plummeted and stabilised from 18% to between 3% and 8%. Property prices soared. Unless interest rates skyrocket, people will keep borrowing, and prices will not fall.

I've never considered interest rates as a driver of boom cycles. That can be seen in previous boom cycles where values still lifted above trend even though the cost of credit was exorbitant by historical standards. I've always considered rates as enablers not drivers. Globally govts relaxed fiscal policy and gave the banksters the green light to lend more. As property prices rose the trend became to access equity and leverage in order to gear up on property. The driver became a loop of equity access + equity increases rinse and repeat. Feeding the frenzy where spruikers that were thicker than fleas on a dogs back.

The primary reason for McKnight's success was this loop. Without this his ability to acquire properties would have been severely limited.

The party never really got going until the late 90's. The big problem is that the 98 – 08 ramp in property prices was too high too fast. It simply out stripped the consumers ability to keep up. Since 10 the markets been flat and will stay so until credit capacity returns to the consumer.

Credit volume (access limitations) and availability (price/rates) are no longer supporting property prices. The consumer has exhausted his/her credit capacity. What little capacity remains is being conserved while they figure out which way national and global economies will trend.

Australia has remained stable and continued to grow albeit much more slowly however that growth came on the back of China's spending binge. Their capacity is now considerably limited. The next decade or so will more than likely see a reversion to the mean on average. Until a new driver of growth materialises economies aren't going to enjoy the boom conditions of the last 2 decades.

alfrescodining wrote:This will be a good year for Sydney's outer suburbs.

Sydney has a lot of outer suburbs from the dirt poor to the filthy rich. It's a bit like saying it'll rain next year.

Good article and interesting comments for both. We are looking at buying our first investment in Midland WA but after reading all this not so sure

I'm not sure what areas you're looking at Freckle but in Sydney where I am the property market is doing quite well, particularly the lower end of the market. Darwin is doing well, Perth is doing well, Melbourne is ok.

I take your point that the property market has risen through times of high interest rates, but the 2004-2007 era saw unprecedented wealth which supported the property market.

However, how many times have we seen interest rates this low and the market NOT boom? None. How many times have we seen interest rates this low and the market DID boom? One. I know the same outcome this time is not guaranteed, but I think it's more likely than not.

alfrescodining wrote:I'm not sure what areas you're looking at Freckle but in Sydney where I am the property market is doing quite well, particularly the lower end of the market. Darwin is doing well, Perth is doing well, Melbourne is ok.You could go to any city and find spots that are "doing well" as you say. You can also find spots that are doing the opposite. This is generally not useful information because by the time a suburb is doing well there's a good chance you've missed the boat and trying to front run hotspots is literally impossible.

The problem with this view is that it is time sensitive. It's all about now or what has just been. It doesn't help you figure out the likelihood of positions in say 5 years. Trends are also rearward looking and are at best a guide.

So to me it's impractical to look at a suburb now that is appreciating and extrapolate from that the market in general is doing well and is likely to continue in this light. Unless there is a broad appreciation in the market of values greater than 5%pa I would have to surmise the market is experiencing some difficulty though albeit some suburbs are seeing reasonable growth.

Quote:I take your point that the property market has risen through times of high interest rates, but the 2004-2007 era saw unprecedented wealth which supported the property market.That wealth was the equity increase due to price rises.

Quote:However, how many times have we seen interest rates this low and the market NOT boom? None. How many times have we seen interest rates this low and the market DID boom? One. I know the same outcome this time is not guaranteed, but I think it's more likely than not.I think you're drawing the wrong conclusion here. While rates have been low on occasion they have not remained low for any great length of time. They may have been part of the over all trigger mechanism but they appear to have played no part in sustaining property price increases.

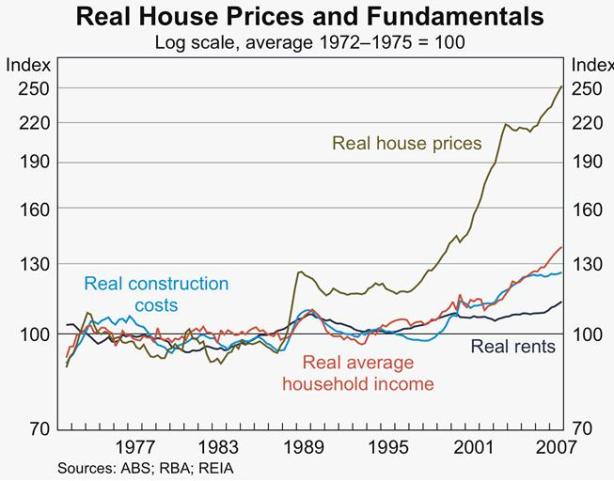

And here's another reason I think Aus property markets provide challenges the average investor would find insurmountable.

A graphic like this screams bubble to me. Simply because the Australian market hasn't corrected significantly yet doesn't mean it won't.

The concerning thing about this graph is that it points to a market that is overvalued by a factor of 2 and that any correction to the mean would see values halve. That's a huge amount of wealth that could be vapourised.

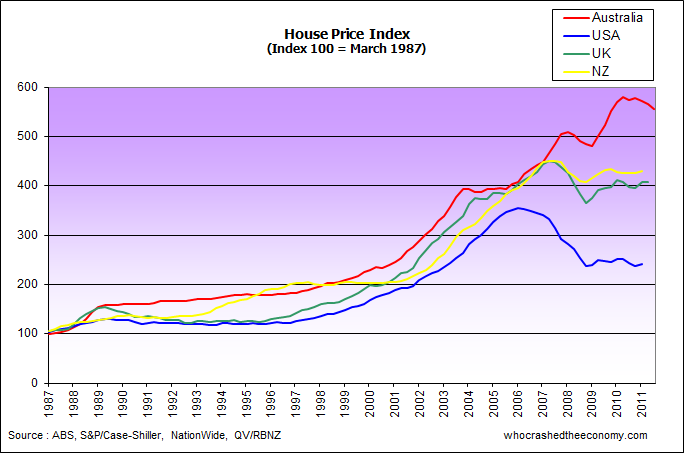

The following graph illustrates how much CG has been the contributing factor to wealth generation. If CG is a thing of the past at least in terms of being able to beat inflation and holding costs etc then one has to question how returns could be seen as reasonable given the trend in rental increases has not matched the level of funds in vested.

This illustrates the difficulty in finding cash flow positive properties when high gearing is employed. When return on capital invested is calculated it obvious that the returns are extremely poor.

While this looks at the traditional buy and hold investor its fairly obvious that investors are going to have to become considerably more sophisticated to scratch a return out of property for the foreseeable future.

Freckle,

Found your frightening article while looking for a graph of interest rates (spoilt my evening

). I’m still thinking about it. But in the meantime I’m refinancing some loans. I would be very interested in your opinion on whether to fix, for how long, and most of all WHY.Thanks

Brian

Brian_qwerty wrote:Freckle,Found your frightening article while looking for a graph of interest rates (spoilt my evening

). I’m still thinking about it. But in the meantime I’m refinancing some loans. I would be very interested in your opinion on whether to fix, for how long, and most of all WHY.Thanks

Brian

Fixing would be based on an assumption rates are likely to rise. Not unreasonable given rates are at historic lows and there are precursors to a rate rise evolving in the wings.

Those precursors are primarily our ToT especially where resources are concerned. The currency wars developing across and between economies isn't helping the situation. The drivers are likely to be imported inflation as a result of CB QE and currency devaluation. If we get imported inflation as well as inflation from a downward currency movement I can't see that the RBA would have much choice but to raise rates. It's probably the single biggest fear that global QE will at some point unleash enough inflation to force rates up.

The other side of the coin is the conditions attached to these types of loans. For that you really need one of the broker boys to give you the ducks guts on that.

Keep in mind what a rate rise might look like. 2% over 3 years might mean an average increase of around 0.7%pa over a 3 year term. 0.7% is going to cost you around $15/wk for every $100k in loans.

There's pro's and cons to fixed versus floating. You would have to model it (best case worst case) to get a reasonable comparison and then fit that into your planning and overall strategy.

Generally speaking fixed is a bet on rising rates and floating a bet on stable to descending rates.

Something else to overlay is the median rent graph. Some bright spark was spruiking their +ve cashflow strategy saying there has been super rent growth due to demand outstripping supply over the past 5 years. Did someone forget about tight liquidity, falling house prices & a gfc?

In some places house prices have increased over recent months. Though medians have risen slightly (Perth etc) volume is down. FHBs are still failing to enter the market, so turnover is predominantly investors.

I'm thinking the money morning article is correct (ATM) Australia may avoid a US style crash and is likely to enter a long Japan style deflation. If this happens, IRs may not be able to rise for some time yet.

Besides, the banks wouldn't be letting you lock for 5 or more years so cheaply unless they were betting on low IRs for that time.

Will IRs get lower? Can they get lower? What does this do to the economy outside of house prices? Can someone answer that?

Phil Soos has just published Super duper graph pac 2 on MacroBusiness

Philip is a research Masters candidate at the School of Management and Marketing, Faculty of Business and Law at Deakin University, and is a researcher for the Land Values Research Group, Melbourne.

http://www.macrobusiness.com.au/2013/05/the-history-of-australian-property-values-part-2/

Of the graphs I found this one particularly interesting.

Strong falls in nominal land values have proven to be extremely destructive, especially when growth turns negative.

The worst on record was during the Great Depression, and the 1990s fall resulted in a recession and the worst financial

allout since the 1890s depression. It again dipped in 2009 due to the effects of the GFC, and is currently at the lowest

point in history bar the 1930s

This ties in with Mirvac (and Stockland) unloading poor performing land acquisitions. Click the graphic for full MB article.

All very good points and I agree with a lot of what Freckle has had to say.

That being said, even IF Australia has overpriced housing/land/real estate, the banks and government will NOT let the prices crash. In fact, we have FAR tighter and stricter regulations in our banking sector than what America ever did.

What happened in the US was driven by bad government policy and horrendous regulations.

In Australia, I believe we do not have this. So yes, even if the market was overpriced (an argument can be made either way) it does NOT mean that we will see massive collapses like what we saw in the US.

Instead we are approaching a time of small movement, or stagnancy in the market. A time where you aren't going to realize massive profits from buy/sell strategies.

The major plan would be to focus on positively geared rentals, which is what we are doing. I would suggest in this sideward market you focus on INCOME rather than CAPITAL GAINS.

SeanWilson wrote:What happened in the US was driven by bad government policy and horrendous regulations.

In Australia, I believe we do not have this. So yes, even if the market was overpriced (an argument can be made either way) it does NOT mean that we will see massive collapses like what we saw in the US.

Denise Brailey would disagree with you.

") ). I’m still thinking about it. But in the meantime I’m refinancing some loans. I would be very interested in your opinion on whether to fix, for how long, and most of all WHY.

). I’m still thinking about it. But in the meantime I’m refinancing some loans. I would be very interested in your opinion on whether to fix, for how long, and most of all WHY.

You must be logged in to reply to this topic. If you don't have an account, you can register here.