All Topics / General Property / The History of Australian property values

Interesting read Freckle.

Yep. This one in particular throws up a few questions about the next super cycle (60-70yrs)

It would pay for everyone to ask themselves, could I financially survive a depression ?

I remember what my grandparents told me about the depression and it didn't sound like fun !

Great read, thanks Freckle.

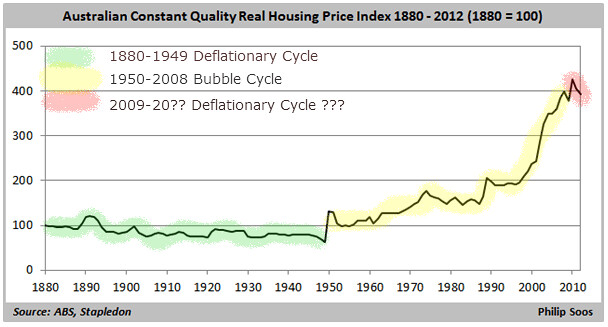

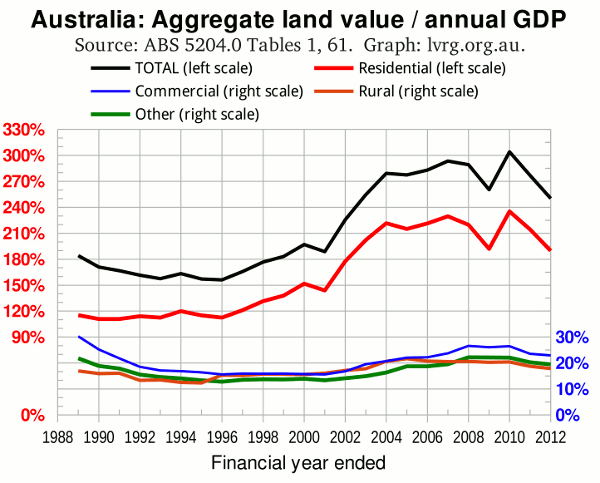

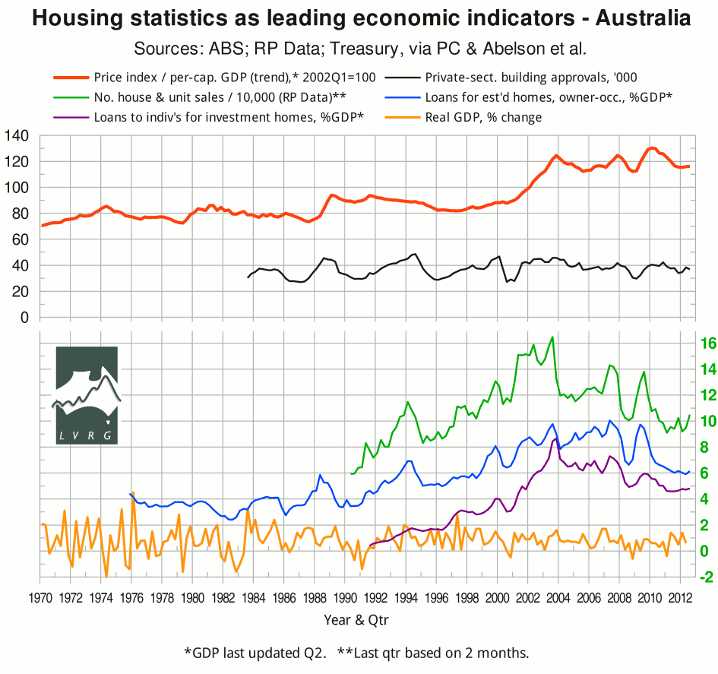

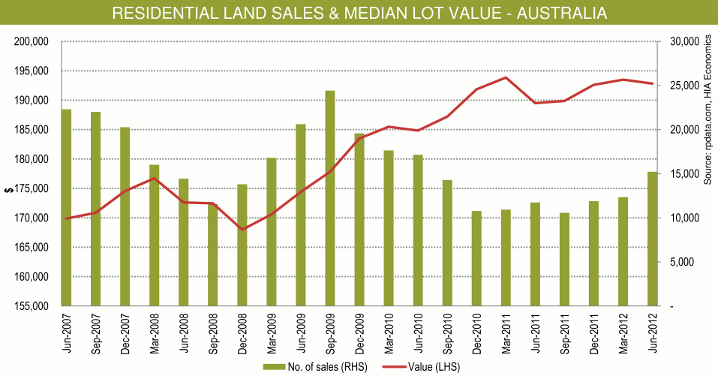

The Land Values Research Group have the odd bit of interesting data

(click the image or image icons if they don't show for graphic and article)

That's a great comment Dubstep and question. Both lots of my grandparents also lived through the depression. From what they told me, the securely employed fared ok.

The article linked to suggests what looms is 4 X as big, however. If it comes apart in a similar fashion, it could well be worse than anything our grandparents faced.

This is scary.. All of the evidence points to certain doom!

I've just got pre-approval for 600K to build my first property and I'm starting to have some major doubts!

minds-eye wrote:This is scary.. All of the evidence points to certain doom!I've just got pre-approval for 600K to build my first property and I'm starting to have some major doubts!

Details??

Things still happen in contracting economies and during serious corrections. You just have to be aware of what your up against and the risks.

Maybe I'm going on a tangent here..

I've been following the Perth vacant land market (<500K) for a few months and it seems like a sellers market right now. Demand seems greater than supply – buyers are getting a bit anxious and paying inflated prices for land. I worry about buying into an inflated market at the peak of the property cycle.

I am agreeing with a lot of people here who say something is going to crash in the next 5-7 years. – not everyone has a mining job and I hear people feeling the financial struggle. What happens when the buyers dry up and refuse to pay the inflated prices which we see today?

I feel like there is enough artificial momentum to keep the prices going for a few years, but I fear what happens when investors get spooked and a whole bunch of supply opens up to the market.. prices will tumble (along with my first investment).

That being said, I'm too new to understand the differences between house and land markets.

<end rant>

Hi,

In 2006, the US house prices reached the highest level. According to Business Spectator, the evolution of the nominal house prices in Australia compared to the US 2006 peak is as follows:

2006: the reference point

2007: +10%

2008: +25%

2009: +18%

2010: +35%

2011: +42%

2012: +37%

The main difference between the US and Australia is that in the US there was a huge over-supply. In Australia, the demand is constantly increasing due to an exponential population and economic growth.

For 2013, Andrew Wilson, senior economist at Australian Property Monitors, forecasts a 3-5% national growth, and BIS Shrapnel managing director Robert Mellor expects a growth between 2 and 8%.

Cheers,

Emil

Sunbuild Invest

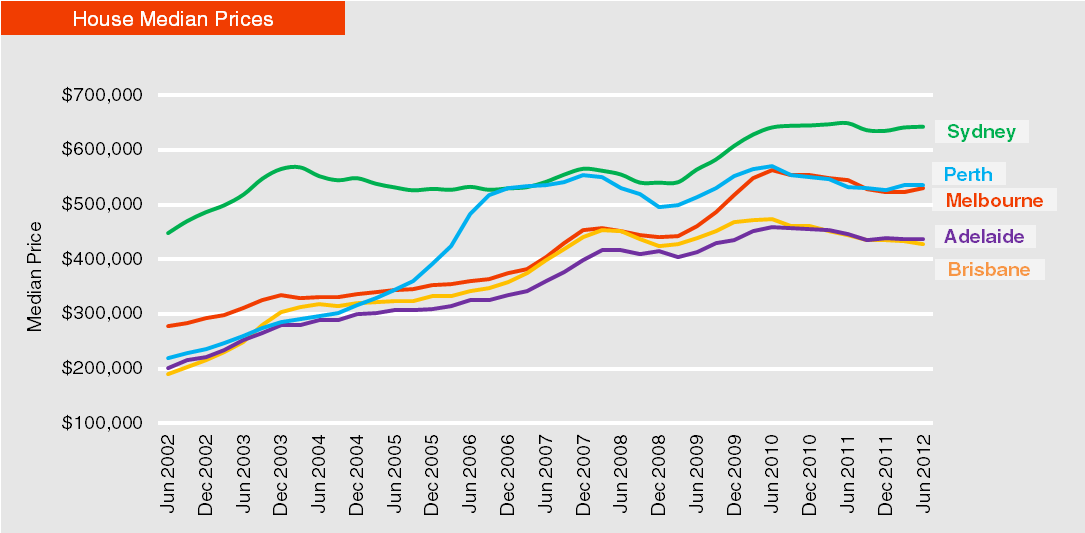

When you look at a suburb i Australia and look at the growth history over a period of around 10 years that will provide a reasonably accurate figure in terms of what the average growth has been and what you should expect over the next decade.

In terms of America it is important to understand that what caused the problem was non recourse lending, what this means is that the loan was only based on the property and it made it hard to go after the borrower. Mortgage brokers in the US were lending to anyone who put there hand up regardless of whether the borrower could afford the loan or not. You see in Australia if a mortgage broker has a client that refinances in the first 12 months they have to pay back the commission. This did not apply in the US so naturally it artificially lifted prices and when the finance started to unravel prices naturally came crashing down.

In Australia this does not apply the nearest example here was what happened in outer areas with the first homebuyers grant, prices were lifted and when the grants came off so did the prices. So if you look at an area over at least 10 years then it should in most cases even out.

Nigel Kibel | Property Know How

http://propertyknowhow.com.au

Email Me | Phone MeWe have just launched a new website join our membership today

nice read, thanks…..fragarcolin

I've never read such bollocks in all my life.

People have been saying this for years.

The fact is, whether by accident or intention, people breed in this country. Household creation drives the property market.

We have a healthy birth rate (compared to other OECD countries) and people are literally dying to get here from other countries.

Demand is greater than supply currently.

Sounds like that article was written by some inner city hipster annoyed that he is having to rent a studio apartment for 2/3 of his salary.

The post-1950's property boom coincides with both massive annual increases in population, and the normalisation of banks lending money for people to buy houses, whereas previously this was not the case.

alfrescodining wrote:Household creation drives the property market.No it doesn't. You can only create a new household if you can meet and access the conditions below.

Quote:We have a healthy birth rate (compared to other OECD countries) and people are literally dying to get here from other countries.Demand is greater than supply currently.

You have a poor understanding of demand/supply dynamics.

Quote:The post-1950's property boom coincides with both massive annual increases in population, and the normalisation of banks lending money for people to buy houses, whereas previously this was not the case.You're getting closer but the population meme is a red herring. The answer is in the second part… banks lending money.

You can have all the demand you like but with out the ability to access credit the demand driver can not be engaged.

Here's an example for you. Arguably there's a high demand for Ferraris amongst males 18 – 40. So why don't we see hundreds on the street. Because only a small percentage can afford to buy one. Provide a viable method for the average worker to buy one and sales will go up.

Pricing, credit and the cost of credit are the primary drivers of property markets. Second to that is credit capacity.

At this point in time we have relatively easy credit criteria and low cost of credit so why isn't the market booming given Australia has a relatively stabile and high population growth? New construction is crashing.

Answer: pricing and credit capacity.

Quote:You're getting closer but the population meme is a red herring. The answer is in the second part… banks lending money.

.

Exactly. And they didn't do it on a widespread basis before the 1950s. Hence the parabolic increase in house prices after that era, which scaremongers like you call a "bubble".

Quote:Pricing, credit and the cost of credit are the primary drivers of property markets. Second to that is credit capacity.

.

That's obvious. People have access to money and credit – much more than they need. Nothing will change that in the immediate foreseeable future. The massive boom from the late 1980s to now coincides with A TRIPLING in people's borrowing capacities, due to structurally lower interest rates, caused by the adoption of sound monetary policy including inflation targets and the RBA charter, as well as deregulation of the economy. The massive price increases are justified.

Quote:At this point in time we have relatively easy credit criteria and low cost of credit so why isn't the market booming given Australia has a relatively stabile and high population growth? New construction is crashing.

.

Were you asleep in 2009? Or when rates were cut after 9/11? What happened last time interest rates were this low? The market boomed. And its happening again. Are you asleep now? Wake up pal. While you're sitting on the sidelines afraid, rational people are making money.

alfresco wrote:That's obvious. People have access to money and credit – much more than they need. Nothing will change that in the immediate foreseeable future. The massive boom from the late 1980s to now coincides with A TRIPLING in people's borrowing capacities, due to structurally lower interest rates, caused by the adoption of sound monetary policy including inflation targets and the RBA charter, as well as deregulation of the economy. The massive price increases are justified.I had to laugh at the sound money quip. I don't think we've seen sound money since 71

Since we went off the gold standard and CB's got the all clear to print markets have become increasing unstable. Post GFC08 they're as unstable as they've ever been and continuing to deteriorate.

Private debt has been channeled into housing as a matter of Govt policy to give the public the impression of prosperity without the govt having to do the hard lifting through fiscal policy. Govt has deleveraged giving the impression of sound fiscal prudence while allowing the private sector to go on a debt binge.

Post 71 govt's lost control. Inflation went parabolic.

Govt's countered with equally parabolic interest rates.

Property boomed and bust cycles continued

The booms preceeding GFC08 match the high spikes of inflation and interest rates. The cost of money (interest rates) does not appear to have affected the property booms of past.

alfresco wrote:Were you asleep in 2009? Or when rates were cut after 9/11? What happened last time interest rates were this low? The market boomed. And its happening again. Are you asleep now? Wake up pal. While you're sitting on the sidelines afraid, rational people are making money.Not really seeing a boom here. For the last 10 years the average compounded return has been around 7% annual. Sydney is half that. By Jun 2010 the market had topped and has been in a sideways to down movement, basically drifting. The funning thing is we have the lowest RBA rates ever 3%. As this continues that 7% growth aggregates downwards.

So why isn't this market booming as you claim?

Was I asleep in 2009. Don't think so. In 2009 I was banking $250k /yr what were you doing?

If you bought property on the rise in 2009 you sure as hell weren't banking $250k/yr. My guess is that given purchase costs, hold costs, probably a good chance the value has drifted sideways or even slipped plus exit costs there's a good chance you're sitting on a paper loss right now.

I don't really sit on the sideline unless I've made a bucket load of cash and I'm looking around for something to invest in. Actually that's what I'm doing right now.

I'm down 40k on silver resources stocks at the moment. I've got a 5k bet with a buddy I'll be up 100k by the end of the year. So if you think I'm a doom and gloomer who sits around fretting about the world and is too scared to get his hands dirty you haven't understood a word I've been saying and your understanding of investment has some way to go yet before it matures.

I did the property thing years ago and I do other stuff now. I'm not after penny ante 8% annual returns anymore. I start at 100% and work up.

My philosophy works like this. If you want to earn $500/wk then you'll probably earn about that. If you want to earn $2000/wk it might take you a little longer but eventually you'll earn that. If you think $10k/wk is possible and you set your mind to it you'll earn that.

aaaah that's right. you're one of these goldbug types! I remeber that from the Japan thread.

say no more! I hear you loud and clear.

This will be a good year for Sydney's outer suburbs.

You should overlay the graph of the real home price index with the interest rate graph. Look from 1990 onwards.

Interest rates plummeted and stabilised from 18% to between 3% and 8%. Property prices soared. Unless interest rates skyrocket, people will keep borrowing, and prices will not fall.

You must be logged in to reply to this topic. If you don't have an account, you can register here.