All Topics / General Property / Property bust not here yet … worse to come

Agree but the US is beyond that. If they cut all discretionary spending they sill couldn't balance their budget.

This is what US total debt looks like. This does not include future liabilities like aged care, medicare/medicaide, pensions etc.

The US is trapped in a debt hole so big it can't climb out of it. Their solution is to dig the hole deeper until they disappear.

There are few ways out actually. Most known is German Style (1946) aka hyperinflation. You can have controlled inflation and just let the time do the job.

Just thinking here, state is no different to private individual. How many ppl do you know that have debt 400% yearly wages?

I know many who is at 800% of non business related debt! No one is going bust, only few.

From the start of GFC, almost 5 years have passed. 5 at say 3% inflation, we devaluate the debt already by some 12%?

Not trying to say I am right, just wanting to hear some opinions outside the box.

Hyperinflation only destroys local debt not debt owed externally. It also destroys the debtor if the debtors income/assets remains at pre hyperinflationary levels which they usually do.

So for example debt owed internationally still remains because it is valued in the lenders currency which will have moved against any hyperinflationary currency.

From the start of GFC, almost 5 years have passed. 5 at say 3% inflation, we devaluate the debt already by some 12%?

The debt has only deflated if your income has inflated. Inflation in prices (costs) and not in income is of no value. Inflation only affects part of your income relative to debt. So if 30% of your income goes to debt servicing but 64% is spent on things that have appreciated then you are not necessarily any better off especially if inflation is or has outpaced your income.

Post WW1 Germany was required to pay reparations in gold. Once its gold reserves were depleted it entered an inflationary spiral that led to a collapse in confidence in its currency. That resulted in the birth of Nazi Germany. Hitler's so called economic miracle was an illusion and by 1939 Germany was about to default on its loans. To avert economic collapse Hitler invaded Poland and immediately went after its gold reserves. Subsequent invasions where not driven by military imperatives but a need to acquire the gold reserves of neighboring countries. Norway was able to remove its gold reserves to England for safe keeping for the duration of the war.

Hope that makes cents… I'm on me 6th burbon..

OK, let's look at it from other side:

Say in Australia, if nothing dramatic happens and economy continue it's trajectory. As time moves forward, people/businesses gradually reduce debt (we are according to statistics already doing it in private sector). Government to reduce spending to match income, as already starting to happen. I cannot see why such a scenario not going to allow a country's economy to re-balance itself over time (say 10 years). I know the risk of deflation is there due to everyone reducing expenditure.

I have noted, that disregarding low nominal inflation and turbulent times since GFC, government still regularly rises minimum award wage. Almost ordering the economy to maintain some level of inflation. That coupled with relatively high by international standards interest rates, seem to run economy at constant inflation.

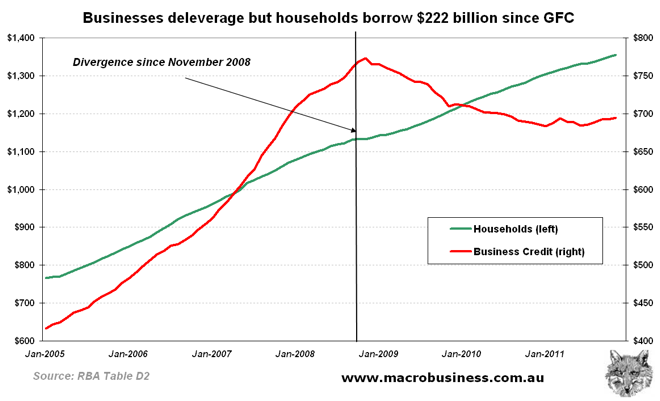

The idea that we are reducing debt and deleveraging is somewhat of a myth accept for businesses that have strengthened their balance sheets since the GFC.

Australia has two significant problems namely; the amount of debt owed to foreigners and that a significant portion of that debt is household debt. A substantial devaluing of our currency worsens that debt profile significantly. We are vulnerable to an external financial shock to a degree most are unaware of. Given that something like 60% of foreign debt is tied up in mortgages (housing) that suggests that the property market carries substantial risk until this mess is sorted out.

Personally I think our chances of this being resolved without a collapse of some sort are slim to none.

$187.6 billion, out of a total $223.3 billion, at end December 2011.

A new all-time record level of indebtedness to foreigners:

Simple,

We have just successfully negotiated an offer from a Qatari company to buy half of us. Its now a deal subject to DD with a cash settlement in 6 months. Fingers, arm, legs crossed on this one. Cant say anything else about it but happy days if it comes to fruition.

Heading off on my trip on Saturday and will post on impressions form out there.

Looks like all is good with the property market bottoming out as far as I can see. Chuffed to bits about lots of my loans coming out of fixed rates and then back to reduced variable, that coupled with high rents makes the holding costs much smaller. I am sure that I am not the only one that is improving their cash flow simply by holding.

bardon wrote:Chuffed to bits about lots of my loans coming out of fixed rates and then back to reduced variable, that coupled with high rents makes the holding costs much smaller. I am sure that I am not the only one that is improving their cash flow simply by holding.Yes vacancy rates are dropping and rents do have some upside albeit limited. The downside will be pressure on asset values as CG goes negative for many while costs rise. The next stage may well be inflationary and job security pressures on tenants. I expect to see PM become more of a challenge and a rise in delinquency rates over the next few years. I also expect to see only a small percentage of PI's manage a lift in their net bottom line over the next few years. The majority will fail to evaluate their investments realistically or critically and make the necessary adjustments.

Second half of 2013 I expect to see WA get a serious wakeup call as the construction wind down enters its final stages.

Prediction for 2013/14. FMG struggles as ore price drops below $90 and a production glut hurts production volumes further limiting GTO. FMG becomes a takeover target.

Oh boy, this is an OLD thread.

Let's throw some fun article in. Source

Slump looms as a third of new home sales abandoned

Melbourne's outer-suburban property market is facing a serious slump as distressed buyers and builders cancel one in every three new home purchases.

The collapse in sales could have serious repercussions for the state economy and the building industry, which employs more than 250,000 Victorians.

"We've never seen this before, so it's a very strong signal that the fundamentals are wrong," said Colin Keane, director of analyst group Research4, who compiled the new research.

<moderator: have deleted pasted text as it was too long. Please see article as linked above. Thanks>

The open house inspections I done over the last few weeks starting to look like "Freckle" scenario.

Owners purchased in 2007 for $845K, trying to get $745K. Two couples on the open house.

Owners listed property for $400K, few months later still there listed $365K. We are the only visitors at open house.

Had 2 open houses at same time, 11am. Both agents been calling me at 11am insisting to see the property. I choose one, and it was lonely walk thru a nice house.

The trend is fascinating, as I use to get very unhappy agents on the phone by calling them Saturday/Sunday. How, they offer to come out and show me the property anytime?! Love the newly found customer service.

So, while RP Data show us 2% drop in values across Brisbane, vendors commonly discount well over 10%.

Market is bumpy, some properties go under contract in in matter of one-two weeks. Other hang around for ages and discount a lot. High end properties are now sold with large discounts. $1M plus houses in Ascot coming up for sale weekly, some are 'special' in the way that been done up very nicely and have not seen market for a long time.

My take of the future if current trend continue: Slow meltdown of RE over the 5-7 years.

The crash started before this thread started but the eternal optimists and chest betters couldn't allow their over inflated PI ego's to countenance such a thought. Heaven forbid. What would their PI peers think of them.

Crashes start BEFORE things go wrong. There are obvious signs if you're prepared to look. All crashes are proceeded by good times. Understanding that a crash is coming is recognising the system is being loaded to infinity. As you stack straws on a camels back you know absolutely that at some future date you will reach a breaking point.

In todays world we try to ignore reality so organisations like governments put props under the camel and lets load it some more. Pretty soon PI's get the idea that the camel will never break because somebody will come along with a solution that will enable the camel to take more straws.

I cringe when I read threads from newby hopefuls oblivious to the current economic climate who are blindly led by those who should know better into committing 110% of their economic capacity on an investment that will return little or slightly above inflation if they're really lucky.

They're just fodder for the economic mangle. But hey somebody's gotta be holding the bag when things turn to custard… right!

Seems to me the simple version of what Freckle and Simple are posting is something like:

The Oz government is fine and not carrying the debt levels of somewhere like the US. Private debt is pretty bad (mostly corporate and individual household debt). This debt is owed outside of Australia.

The question Simple poses is can the debt be ridden out until things are on an even keel. It does seem possible, say if house prices stagnate for 7-10 years and there is no real growth in business debt. But, the big but with this is, how does this allow wages across the board to grow at even 3% PA?

Australia's consumer economy is so used to 'equity mate'. How do other sectors grow if equity is not?

If it stagnates and become stable, it will still be bumpy and painful for the most indebted. The flip side is property takes a hit, as Freckle suggests.

2007 was kind of the national peak. 2008 shaved a bit off the top. The Rudd handouts and FHOG boost (probably more to help his wife with her investment property than anything else:)) only served to get prices back to the peak by 2009/2010. Since 2010 the market has not been healthy but it is only really this year that concern seems to be becoming widespread.

Who knows what's going to happen. I have been saving cash and waiting. It's getting close to the point where buying would cost me no more than renting – but IRs are unreasonably low. I like to factor in a spend at average IRs of around 10%, rather than the current 7-8% most banks are offerring.

Freckle – who is holding the bag now is very important to how it unfolds in Australia, I believe. From what I understand, the greater majority of IPs are held by those currently in the 55-65 range. NG has been their friend but now this age group is starring down the barrel of retirement (forcibly in some cases).

Stock on the market is going to grow. Eventually, many sellers will become desperate. What happens then is what decides whether we crash or stagnate.

To add one more variable to the discussion, consider that since GFC 2008, the age group 55-65 are also same people that had to stay in businesses to continue working. This is due to sudden drop of revenue and evaporating retirement savings plan in some cases knows as (SUPER fund losses).

They are now have worked extra four years in business trying to recover and stay afloat. As Ummester mentioned, time is running out for them, and they will give up on various grounds with in next 5 years (mainly health and capacity).

They will not be able to sell the businesses for same $$$ as pre 2008, profitability have dropped. And a lot less people with cash to purchase.

They are the same guys that hold multiples of IP's in Australia. They are your 5% of people that own 3 or more IP's. They now will need cash to support established lifestyle and increasing health bill. Selling IP's will look attractive, when you know you got 10-20 years left.

As a summary, I see multiples of downward pressure factors. I also, do look for supporting factors, but they are hard to come by. Willing to help me to update my list of positive/price support factors?

Thinking only about Major Cities:

– Inflation will support pricing

– Population Increase will support pricing

– Time factor, will allow economy healing. Will support pricing

The government and RBA will try to support pricing, possibly offering stimulus and definitely using IRs as a blunt tool, to help the balance sheets of the big 4. No one wants to see an Ozzie bank go down, so their integrity will be defended as much as possible.

I think the Australia economy is already in a recession, I think people who do not think this are delusional.

If you look at any global economies there has been ups and downs for the last hundred years, Where in a down period, Freckle has pointed out one thing though that is very interesting, The amount of people with HOUSE HOLD DEBT is incredible.

Im a GEN Y (28 Years OLD) my debt is this: My car KIA RIO (gets me from A to

at $77.00 per month on lease, House loan: $90,000.00 + two good incomes.My of my mates 28 to 38, average mortgagee 400k+, credit card +++, personal loans+++ , Harvey norman two years interest free (two years are now up), car lease 1000+

Four mates of mine lost their jobs these two income families when into one, and they are screwed, Bills can’t get paid, etc” What worries me is this, two of the four and I sat down had a look at the numbers and it looked very worrying. The problem is that its not only 4 mates of mine going through this, A large number of the population.

To top it off the next time you go into a retail store ask the shop assistant this, Are people using cash, eftpos or credit cards Most of them would say credit card cards, The amount of people who use more then 1 credit card now is scary!!

Jpcashflow | JP Financial Group

http://www.jpfinancialgroup.com.au

Email Me | Phone MeYour first port of call in finance :)

Well, I am actually on opposite side of the fence. We hire people, run manufacturing facility.

Since 2008 we lost turnover, dismissed 25% of our staff. Our competition went of business (bust), our clients take 2 years to pay 60 day account.

None the less, guys that work for us on $25-30/h carry new Iphones + Ipads + drive $30K+ cars. They also go on holidays and renovate houses. I think there is some degree of disconnect with reality and lack of observation.

The fact is, we are likely to see more pain. 4 days working weeks very well can be an option mid 2013. When I mention this to our staff they look suprised, walk away and continue the trend.

If economy nosedive anymore in next 24 months, I can see many people not been able to meet the financial obligations AKA look out for repo sales.

I think the most important thin is each person has there own personal econmy, recessions have always been around. But there are always opportunities

Jpcashflow | JP Financial Group

http://www.jpfinancialgroup.com.au

Email Me | Phone MeYour first port of call in finance :)

I think that in a down market also creates opportunities. I can see that a city like Brisbane is currently under valued.

I do not like boom markets its a little like being on the set of the walking dead. People over pay because they are worried about missing out. In a market like this if the deal works then in the medium term you will make money

Nigel Kibel | Property Know How

http://propertyknowhow.com.au

Email Me | Phone MeWe have just launched a new website join our membership today

") at $77.00 per month on lease, House loan: $90,000.00 + two good incomes.

at $77.00 per month on lease, House loan: $90,000.00 + two good incomes.You must be logged in to reply to this topic. If you don't have an account, you can register here.