Forum Replies Created

- kong71286 wrote:And with many experts predicting +$50 this year I am very excited about being part of this BULL market

Yup Silver has been a bullet for 7 months. Expect some buying opportunities during significant pullbacks (if you are confident it will run in the medium to long term).

I too prefer the more nimble investment opportunities presented by commodities over property currently. I think rising commodity prices will increase inflation eventually globally. This will slow economic growth, no matter what interest rates do.

Hi Beedie, I doubt I'll go to Steve's market update in Brisbane on March 9.

I honestly don't see any data that changes my earlier views.

I am not interested in passive property investing currently because I don't think future CG or yields will be competitive against other investments.Jason, there's undoubtedly regional opportunities due to commodities export growth. However, I wonder whether lenders will do 85%+ LVR on them, and what time frame represents a reasonable risk? I delved into Qld coal town opportunities in 2003, and came away thinking the risks were not worth taking. The mines, LGAs, and select locals seemed to have too much power and a very asymmetrical information advantage. Unless I was privy to the same info, I'd prefer to steer clear. I don't see the same investor appetite today as 5 years ago, to flick mining property to after holding for 12 mths. Further, we already have CIPs in the Isa and the PMs and services up there have dealt some real gotchas. Mining town PMs make a specialty of milking absentee city LLs. After all, their cost of living is as high as the miners if not higher, and they want their bite of the beef.

Because of my essentially stagnant impression of property prices for the next 5 years, I've peeled back on following the monthly data. Nevertheless, I'll try and get some charts up for and against my view, in the next few weeks.

My energies have been focused on "trading" commodity volatility for at least 9 months – palladium, silver, rare earth elements, and lithium. and getting some health and fitness back after several years of sitting at a computer for way too long.

AUSPROP wrote:oh is this where everyone has gone. maybe Dazz could be enticed back here…. full circleHey AP. No, not everyone came here. Only me it seems.

I think Bill.L posted on the new Australian Property Forum a while back.

Dazz isn't active anywhere I am aware of….probably off building his real world empire.

And Sunfish is back on Somersoft.I occasionally skim the topics at SS to gauge permabull sentiment….but am spending most of my net time improving my understanding of commodities and global equities, stuff that property permabulls have no interest in cos God told them no matter what happens in the rest of the world, property always goes up

")

edit:

Happy New Year Michael. There should be some ripe opportunities coming up in 2011 for the wise man. Was talking with a Nundah (northern Brisbane suburb) REA at a party last night. He reckons more builders are unloading their development sites cos it is hard to get dev't finance without significant cash flow from other avenues.Happy to put you on to him when you are ready. He is a young fella (been an REA for 10 years) but his family have been in the area for 30+, and he knows everyone.

Hi Mr Michael. In 2011, I'll continue to read widely and deeply on what really drives house prices, and post about it.

I want to come to a better understanding of money, credit supply, and the effects of banking deregulation. Several at Somersoft (High Equity, Tom) had reasonable insight, but imho fell into the trap of thinking that foreign credit money is somehow different to real money (because it is owed back to the lender). I could accept that if it didn't effect demand for goods (houses) and services.

May all your attainable New Year's resolutions be attained.

What's happening with housing supply??? Well,

– NSW cannot beat pre 2004 levels.

– Vic is still rising, thanks to greenfields being released after the govt did a 180.– Qld is still down after being kicked by GFC.

– SA is busy providing houses for all the locals who are now not moving to Qld.

– WA is falling off a cliff for the second time in 3 years.

Housing Finance Commitments

The trends for Qld and WA are a lot weaker than NSW and Vic.

Qld commitments have dropped to 2001 levels and WA to 2000 levels.The decrease in commitments since preGFC are:

NSW 27.5%, Vic 13%, Qld 33%, WA 31%Charts from Aussie Macro Moments

Total listings is quite revelatory regarding the weakness in the Qld market. Considering the smaller population, Qld now has more listings than Vic and NSW.

I'd say this has something to do with the discretionary nature of the Sunshine, Gold and Fraser Coast markets, and the more recent weakness in Brisbane.

There's no doubt the softening has been national since September 2010.Note the chart heading should read Jan07 to November 2010

All charts from RPData

Qld and WA lead the fall in building approvals. Has to be due to the banks not wanting to lend in Bris and Perth moreso.

If prices stay flat or fall, at least rental yields improve quicker.

FHB activity is stronger in some states than others. In order of strength : Vic, WA, NSW, Qld, Tas, SA, NT, ACT

Population Growth

Slowing

because of net migration

NSWers have had been flooding into QLd for years, but have slowed since March 2009. This presumably accounts for much of the drop in Qld house prices.

Nevertheless, pop growth in eastern states is still historically strong.

Beedie, of course, the best fiction is based on true life

I can see the govt will eventually yet again have to intervene to stop house prices dropping dramatically in a short period…..presumably when foreign credit contracts, even moderately. ….that means another govt backed guarantee for Aussie bank foreign borrowing.

Socialize the losses, and privatize the gainsHmmmmmm…..

Moving on, I've been messing with some charts. I've always felt number of finance commitments was possibly a slight leading indicator of house prices.

Below is rolling Annual % change in total Australian finance commitments versus rolling Annual % change in Sydney house residex index

I have to go away and contemplate the smoothing and lag effect introduced by rolling annual numbers…..but at first looks, correlation seems reasonable.Eventually, I'd like to account for most house price movement. My guess is interest rates and unemployment. have historically accounted for most of the influence.

Though looser lending standards since banking deregulation will have muddied the waters.beedie wrote:WW I have a strong suspicion that we already there my friend …… from my own and my different contacts personal experience with properties on the market at present

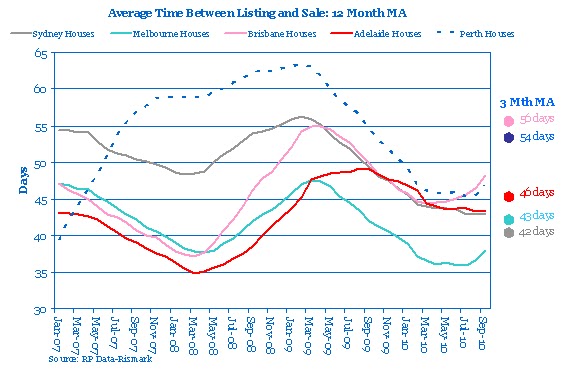

For any one interested have a look on this site. It’s a guide to days on the market http://www.refindhouseprices.com/

Thanks Beedie. I suspect you are right that it is already >55 days.

I have RPData which is essential when making offers imho. Gives advertising history week by week, for sales and rent.

Though refindhouseprices is a bit easier to skim a lot of houses in a burb.Here's a silly story.

Consider we have oafey slow thinking do gooder ideologues in the RBA and Fed Govt who finally realize affordability might be an issue.

So the RBA decides it will now consider asset price inflation in setting the cash rate.

Hmmmm……ok, so house prices too high -> raise rates, even if conventional inflation is within the target band.

Hmmmm again…..that decreases the amount buyers can borrow, and increases the cost of building new stock.Population growing at 1.5-2%pa.

Housing supply drops below 30,000 per qtr.Hmmmm indeed.

Dan42 wrote:The 'Housing Commitments v IR' is really interesting. Goes to show that it prices could be severely affected without huge rate rises. Next year should be very interesting, especially if rates rise as predicted.

Thx Dan. I should have put median prices on the same chart. I think what the 2004-2007 anomaly represents is the further loosening of credit standards such as LVRs, DSRs, post codes, and documentation. I'd posit this overwhelmed the tightening effect of rate rises. I'd say lenders were able to continue sourcing large amounts of foreign credit, and were resisting the RBA's attempts suppress credit supply via higher rates.Also, the relistings graph backs up what we've been seeing locally. The Adelaide market has about 40% more houses on the market compared to the same time last year. The Real Estate section in Saturday's paper was so big I almost put my back out lifting it off the table!

Appreciate the Adelaide on the ground picture. Listings are up 50-100% in Brisbane outer and mid ring burbs, though vendors are yet to drop prices significantly. I expect downwards pressure to build in autumn next year. And that's when I might be making low ball offers on development sites. Nevertheless, I'll be following the rates outlook.

The chart below is the ASX's 18 month forecast on the Aussie cash rate. Only another 2 x 25bp rate rises built in at this point, but then bank cost of funding could still increase beyond that, as it has been.

When Australia's premier skin in the game property permabull Chris Joye changes his tack (from ever upwards), you have to believe the market isn't going up in the near future. Some of his recent charts showing the market has flatlined.

I don't know of any free data showing cap city 'time on the market' (and REAs are secretive about such things) so am grateful Chris published this.

My on the ground research says Brisbane's moving average will blow out beyond the GFC 55 day peak in the next 3 months.

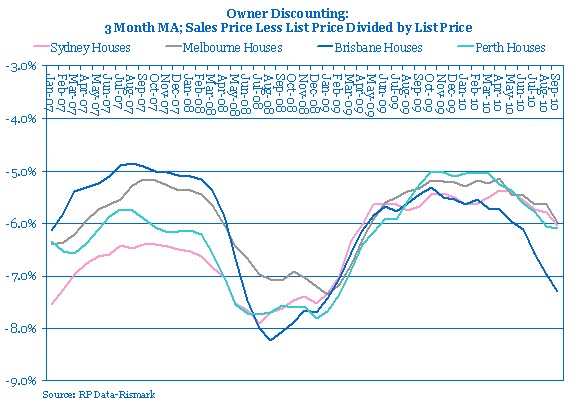

Another valuable chart from Chris' RPData – the discount on list price a property is sold at.

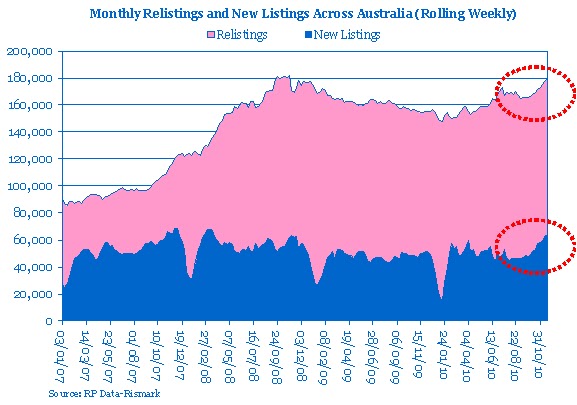

Relistings are now as high as at the peak of GFC, while new listings are fast approaching a 4 year high.

Usually there's a seasonal drop in new listings in January. The extent of the Jan 2011 decrease will be telling.

This is an interesting chart of housing finance commitments and the standard variable interest rate inverted.

I've inverted the rate to more clearly highlight the negative correlation between rates and prices, that is prices move down when rates move up.

Interestingly, the green shaded area of the early noughties, is the only sustained period of prices moving up in the face of rate hikes.Note the unprecedented higher frequency and amplitude of negative month on month growth in Brisbane's median value.

It might be expected considering the unprecedented growth in the early noughties and that prices have to eventually revert to average debt serviceability and wage growth.thx beedie. I see cap city property growth averaging -5% to 5% pa in nominal terms over the next 5 years.

will all depend on cost of foreign credit, which I expect to tighten eventually.

But that doesn't mean I am a permabear. I'll be keeping an eye out for distressed sellers, particularly on Somersoft forum, and buying something that adds value.

Passive property investing isn't my game.IP Freely, the variables I used are mentioned in the post. but maybe I didn't express it clearly. For paye tax, cgt, etc, I used 2010 figures.

Why? The purpose of the model is not to accurately reflect B&H gains over the last 30 years, but gains of the next 30 years. Long term B&H spruikers like the Somers believe their strategy is as valid today as 30 years ago. they must therefore believe modeling on the last 30 years of economic cycles is more valid than random generated cycles.

Of course, 30 years is a long time, and anytthing could change – negative gearing could be messed with, 50% cgt concessions could be lost. Stamp duty could go right up on investment properties.

I once discussed the advantages of a timing model with a sharp Somersofter many years ago. Both our models indicated buying property at the beginning of a bull run and selling at the end, then swapping into the share market and cash, gave superior after tax returns.

I am happy to see others model this stuff. Some of my gurus are the people at Pimco. and they believe the new normal is B&H is dead. I tend to agree. There's too much volatility and too much debt. Maybe someone will do well over 30 years, but the risk associated with holding all that time will be much higher in my view. and it is all about risk adjusted rewards in my book.

Thanks Ben, appreciate you saying that.

And hello LR. Good to see you here keeping the b's honest.

Yes, KeithJ, Sim, and puppet cheer squad must be smurking loudly after finally getting rid of another motley crew of independent researchers / thinkers incapable of mindlessly ramping property.

Their Lord and Master has taught them well – "It doesn't matter what happens to property values after I die, as long as they go up up up so I can eat lots of cake then play skip rope to burn it off. Noblesse oblige is for suckers".

No longer will Sim have to stay up late into the night waiting for computer alerts signalling yet another post with the unmentionable 'soft', 'flat', 'crash', nor worry if some not so random forumite is playing "My stats are bigger than your stats"

And, I presume they've been summoned by his Lordship for high tea, a swim, and a spot of tennis overlooking Moreton Bay from the foreshore of Cleveland in Sunny Qld, for a routing job well done.

Meanwhile, I am wondering more each day when the Somers are going to publish their 'bigger stats' to validate their 30 year old message is as relevant today as when we didn't need to borrow so much mulah from foreigners. Must be a whole new generation they can sell their message to, and seduce ever more fresh blood/debt into "The Great Game".

beedie wrote:Agree in the fast turnover approach WW need to keep the momentum going good times or bad otherwise we do nothing…. and experience tells us doing nothing produces nothing…

agree beedie……..and early birds get the worm….so always ear to the ground re infrastructure changes. a savvy active investor shouldn't see any surprises in City Plan 2012 by the time it comes out.

We focus on LMR sites and will be avoiding Moorooka next year .. feel a bit of a glut happening there…. we have a complex of 6 on the market there now…. and our builder is weeks away from finalizing 16 of this own around the corner from us and sales on both are relatively nonexistent .

Agree re Moorooka glut. Have noted at least 4 new complexes hit the market in the last few months. Every man and his dog have been all over the burb in the last 2 years.As far as Cross River Rail goes… got a bit excited at first as have another property at Yeerongpilly (thought of density increase).. Then read all about it …link below

Will read up on that. Have been trading commodities moreso since May.Such is the speculative cycle

Hmmmm…..not so much speculation….more trying to match supply to demand at an affordable price within the restrictions imposed by slow moving govt.Us QLDS need to keep in touch and as far as Somersoft well think they lost one of thier gurus…………lol

ha….actually there used to be some sharp pencils on the site who i enjoyed exchanging xls models with, but they've moved on. There seems to be only one or two who do MUDs…….otherwise all cosmetic renos, passive B&H, duplexes, and speccies.

Qlds007 wrote:I do agree however i think the opportunities will increase if you hang and wait your time with a few more rate increases.Thanks Richard. Fast turnover will be the first thing we'll be looking at next year, maybe a quick corner lot boundary realignment and flick, uncomplicated by a slide. low risk low cost stuff. They seemed popular around Banyo, Zillmere, and Goodna over the last 18 mths. I've noted more recently LMR sites were being churned by small developers in Moorooka and Salisbury, but bidding was pretty healthy at the three auctions I attended.

We may take an equity hit on two properties we've bought this year (Grange and Wavell Heights), and the PPR we have for sale now (Highvale) but appreciate the opportunities ahead, contrary to one too many dills on Somersoft who think anyone who recognises a market downturn is a doom and gloomer.

Two infrastructure projects that have to be taken seriously are the cross river rail and Petrie train extension to Mango Hill (?Redcliffe) Both should be accompanied by denser zoning in appropriate precincts.

Yes I am in Brisbane. The slow down seems to have been more pronounced and early here than Syd, Cbr, Mel.

Be interesting to see how things unfold in the next few months nationally.duckster wrote:Winston – People (the herd) only know that Property only goes up –Yes, a lot of people (especially over at Somersoft) are punch drunk on the last 10 years of growth.

I wouldn't touch a Brisbane site that could not be developed substantially (unbeknownst to the vendor) at the moment. Listings in Brisbane have gone up on average 50% in the last 12 mths, and 100% in some suburbs.

Will keep my gun powder dry until after another couple of rate rises next year.

How anyone can think Australia doesn't have a two speed economy is beyond me. Just go talk to your local shopping centre small business people, and see if they are saying the same as Marius Kloppers and Tom Albanese.

")