All Topics / Finance / Depositors dont complain about your current low interest rates

In the clearest signal yet that we are still in a potentially devastating global deflationary spiral, The Riksbank, Sweden’s central bank and the world’s oldest central bank, has effectively cut interest rates to minus 0.25% and has started a program of quantitative easing a.k.a printing money. These are the most dramatic moves yet by a major central bank and will be watched the world over for signs of success or failure. Let me explain what the Swedes are doing and why.

On 2 July 2009, the Riksbank unexpectedly lowered rates across the board. Economists had expected the Riksbank to keep the repo rate at the low 0.5% level. The repo rate is the official bank rate at which banks can borrow from the central bank against government bond collateral. It is the floor rate, the lowest rate in the banking system. But the Swedes lowered the rate to 0.25%, a record low.

The interesting bits were buried deep in the accompanying press release, namely that the Riksbank was to engage in quantitative easing and to penalize banks for holding reserve deposits.

The weak development of the economy requires a somewhat more expansionary monetary policy. The Executive Board of the Riksbank has therefore decided to cut the repo rate by 0.25 of a percentage point to 0.25 per cent. The repo rate is expected to remain at this low level over the coming year. At the same time there are several signs that economic activity will improve.

Deep economic downturn

Economic activity abroad is very weak and this hits Sweden hard. Exports have fallen substantially and the situation on the labour market is continuing to deteriorate rapidly. The information received in recent months points to the economic downturn in 2009 being somewhat deeper than the Riksbank forecast in April.

Low repo rate over a long period of time

A lower repo rate and repo rate path are needed to counteract the fall in production and employment and to attain the inflation target of 2 per cent. The Executive Board of the Riksbank has therefore decided to cut the repo rate to 0.25 per cent. The repo rate is expected to remain at this low level until autumn 2010. The Riksbank’s assessment is that cutting the rate to 0.25 per cent will not threaten the functioning of the financial markets.

The Riksbank’s assessment is that after cutting the repo rate to 0.25 per cent it will have reached its lower limit in practice, and that the situation on the financial markets is still not completely normal. Supplementary measures are necessary to ensure that monetary policy has the intended effect. The Executive Board of the Riksbank has therefore decided to offer loans totalling SEK 100 billion to the banks at a fixed interest rate and with a maturity of 12 months. This should contribute to lower interest rates on loans to companies and households.

So, here’s what the Swedes are saying:

- Economic activity abroad is very weak and this hits Sweden hard. That means the Swedes can’t export their way to prosperity because no one is buying. Everyone is in a synchronized global downturn. One subtext, I should mention is that Sweden is greatly affected by the collapse in the Baltics because there was a huge trade flow and banking relationship between Sweden and the Baltics. Therefore, the economic depression there is not good for the Swedes or their banking system.

- A lower repo rate and repo rate path are needed to counteract the fall in production and employment and to attain the inflation target of 2 per cent. Output ad employment in Sweden is so weak now that it is creating deflation. We have to lower interest rates in an effort to stimulate borrowing, which we hope increases credit and ultimately production and employment.

- The Riksbank’s assessment is that after cutting the repo rate to 0.25 per cent it will have reached its lower limit in practice, and that the situation on the financial markets is still not completely normal. Look, we are cutting rates as low as they can go, effectively zero. And financial markets are still not normal. Banks just are not lending enough to create the credit in the system necessary to increase production and employment.

- The Executive Board of the Riksbank has therefore decided to offer loans totalling SEK 100 billion to the banks at a fixed interest rate and with a maturity of 12 months. Because cutting rates, the policy tool we prefer, is not getting the job done, we are going to effectively print money out of thin air. We will start making loans to banks with fictitious money that we create solely to increase the amount of money in circulation in a desperate attempt to increase consumer and business credit, consumer price inflation, and output.

- The deposit rate is at the same time cut to -0.25 per cent. And as an extra measure, we will start penalizing banks for not lending by charging them 0.25% for holding deposits at the Riksbank. Now, they will have every incentive to start lending…we hope.

Pretty aggressive plan, if you ask me. Will it work, though?

Well, first of all, most every major central bank in the world, certainly the biggest: the Americans, the Eurozone, the British, the Swiss, and the Japanese, have rates near zero and are printing money. The world is awash in money and the incentive to borrow is huge. So, is the Swedish announcement qualitatively different? On some level, it is not. Nevertheless, it is the most aggressive policy and the fact that they are charging negative interest rates for deposits is unprecedented. This does make events in Sweden something to watch.

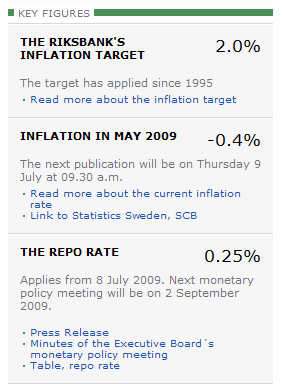

Moreover, the situation in Sweden is bleak. GDP is expected to contract 5.4% this year and inflation is expected to be negative. Clearly, the Swedes are in a deflationary spiral. It doesn’t help that its banks lent recklessly to the Baltics and that those countries are imploding. The Swedish banking system is at present severely undercapitalized – this is why lending is not taking place. The chart to the right from the Riksbank website on key figures sums it up.

Moreover, the situation in Sweden is bleak. GDP is expected to contract 5.4% this year and inflation is expected to be negative. Clearly, the Swedes are in a deflationary spiral. It doesn’t help that its banks lent recklessly to the Baltics and that those countries are imploding. The Swedish banking system is at present severely undercapitalized – this is why lending is not taking place. The chart to the right from the Riksbank website on key figures sums it up.So, the Swedes are lending €printing money. What’s more is they are taking economist’s up on their suggestions regarding negative interest rates. Back in April and May, it was suggested that negative interest rates were the way to go in order to deal with these problems. Basically, you are giving people money to borrow. There cannot be much more incentive than that.

The thing is you can lead a borrower to the bank, but you can’t make him borrow. Do you even want him to borrow. The last time I checked, it was savings and investment which created long-term growth. In my view, people are terrified of over-borrowing now and no amount of easy money is going to change that overnight.

Here’s the problem. I take a fairly Austrian School tack here. Punishing borrowers by lowering interest rates to zero and printing money is not going to solve the problem. The problem was low interest rate and easy money to begin with (and a lack of regulatory oversight never hurts too). This created a binge of reckless lending. We are now seeing the result of that lending worldwide, Sweden included.

What Sweden needs is more capital in its banking system. Remember the whole song and dance about the Swedish solution? Supposedly, the Swedes were brave enough in the early 1990s to bite the bullet and nationalize insolvent banks in order to re-capitalise the banking system and get lending going again. Everyone and his sister was saying this is what America needed to do. I still say this is what needs to be done: punish reckless lenders by liquidating zombie undercapitalized banks but provide enough liquidity at normal interest rates to keep the system intact. And, I am sure taxpayers would be a lot more willing to pony up under these circumstances than under the present policy of giving the reckless lenders free handouts. If you want to prevent systemic collapse, it is the banking system, not the banks, which is important.

But, apparently, everyone just wants easy money and no one wants the Swedish solution – not the Americans and certainly not the Swedes.

Richard Taylor | Australia's leading private lender

That was really informative – thanks

Hi Singer

So next time you pop into the CBA and they tell you that your savings account is only earning 0.005% dont complain lol.

Richard Taylor | Australia's leading private lender

Just a quick thought on legality and context.

This story should carry an author acknowledgement, even if it is almost two weeks old, written about Sweden from an American perspecitve. For the record, tt was written by Edward Harrison's US Blog site Credit Writedowns.

Out of respect for the author and thinker behind this work, the post should also include the authors important footnote out Richards copy and paste. It reads:

"Update 1300ET: Note – so as not to play too fast and lose with my terminology, I should clarify that the Riksbank is charging banks for holding deposits at the Riksbank. They are not lending at negative interest rates as the statement “Basically, you are giving people money to borrow” suggests. Also, regarding the lending by the Riksbank, they are not technically engaging in quantitative easing (buying government paper with new money). However, the net effect of the lending is to increase credit flow."

You must be logged in to reply to this topic. If you don't have an account, you can register here.